I attended the AGM of ESR reit yesterday. It was my first AGM and was an eye opening experience for me. The Reit had just announced their earnings for the 2018 first quarter in the morning and the results were disappointing. Earnings can be found here

The earnings showed that DPU was down by 15.6% from the previous Q1 a year ago, mainly due to their equity fund raising. Gross revenue rose 21.2% year-on-year to S$33.6 million, while net property income rose 20.8 per cent to S$23.8 million. Notably this impacted the mood at the AGM and some shareholders did speak out regarding the issue.

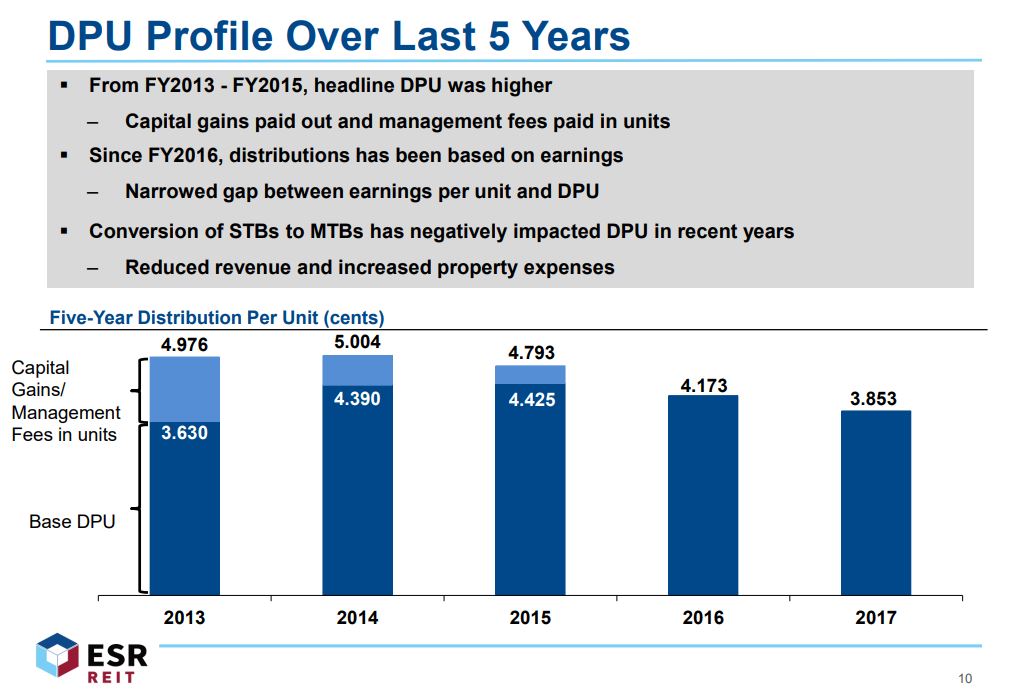

1) SCRIP Dividend policy. Unit holders complained that having a scrip dividend policy that was inconsistent is bad for them as it results in odd lots.

Management replied that since the equity fund raising the overall debt of the Reit has been brought to 30% and therefore the Reit has no reason to conserve cash. The Reit decided to not issue SCRIPs this quarter for that reason. I guess that in itself speaks of the policy.

2) Management not taking their management fees in units. A shareholder questioned if the Reit manager did not have “faith” in his own Reit. Several unitholders also pointed out that a good Reit manager would attempt to “balance” the DPU of the Reit by accepting fees in units during bad times and accepting in cash over the good times. Thus over the long term value is not diluted.

Management replied that it is important for a Reit “not to pay out more than it earns”. By electing to receive management fees in units, the manager is artificially inflating DPU and over the long term diluting the value of the unitholders.

The management also mentioned that they would take this step in the case where multiple properties are going through AEI and over the short term they needed to bridge the DPU. By taking management fees in units now, there would be no avenue to do so in the future.

3) Falling DPU, and the reason behind trying to reduce the gearing at the cost of yield.

Management pointed out that the Reit is in transition and they are still looking for avenues to divest and recycle capital for properties in the portfolio that are worth between 15 – 20mil with low potential upside. In such a scenario, a low gearing for a Reit is actually beneficial as it signals good credit worthiness. For example, being able to hear multiple proposals from sellers of properties and being able to negotiate debt instruments at better rates.

Having a good level of debt means that the Reit is able to look at further AEI’s to improve the existing properties with potential upside and lock in tenants. The low gearing levels also mean unit holders do not just have to rely on the outcome of the Viva-ESR merger to grow their existing portfolio.