This month will mark the 2nd year since I applied

for my BTO. Having just visited the location and seeing the building at mid-stage

of completion, I wanted to pen down some thoughts regarding my financial

housing journey.

For us, our future home was in a mature estate with a good

location and was thus “expensive” for a BTO. I remember being quite anxious

about the overall quantum we had to pay, since we had only just started working.

I had calculated that based on our combined salary then,

even after CPF deductions we would be facing a negative cash outflow when the

house arrived. Yikes!

Desperate to avoid this, I formed a plan to rein in our

mortgage by increasing our down payment. Our goal was to bring the monthly

mortgage payable to under our monthly CPF-OA contribution.

During this time I read many commentaries online that advocated

either paying down as much as possible or paying down as little as possible and

investing the rest. There are well written pros and cons to both, but like any

advice, you have to tailor it to your own situation and personal circumstances.

For me the second strategy made more sense, as a fully paid

off home has no cash flow, and there are many ways to save on interest in the

future including partial payments. Besides, the interest savings on a BTO is

not as significant, especially if you intend to flip it at some point. Thus, I

had to strike a balance between paying down and reducing the mortgage and

keeping enough dry powder to constantly invest.

To do so, my rule was to treat only the asset price of the

house as the investment component. Thus we paid for the option fee, stamp duty

and optional components in cash. I remember at the time this meant a having to

make difficult decisions for fund allocation.

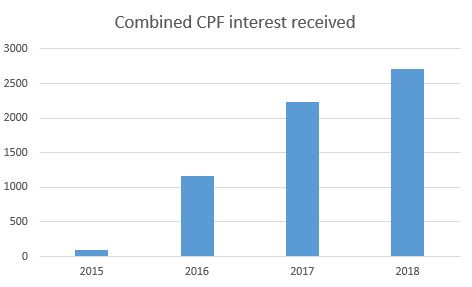

Looking at our finances right now, our combined CPF-OA

balances equate to about 13% of listed value of the home. Which should mean

that we are on track to paying off close to 25% of the value of the house when

it arrives (including 5% already paid). Based on this figure, it would also bring

our monthly mortgage to below our CPF-OA contribution with some change to spare.

Along the way, it really did help that we experienced wage

growth which allowed us to grow the CPF-OA contribution, but this does not

detract from the fact that we had a plan and stuck to it.

While I always advocate for couples to buy homes within what

they can afford, I think it’s also important to have game plan on how to afford

something and looking at the value of the item rather than the absolute price.

Understanding the value of what you are buying is also very

important. I know of couples who bought relatively cheaper flats but are

dragging their feet moving in as the location is not as prime and with fewer amenities

in the vicinity.